February 2026

A control premium is the percentage paid over the minority-interest value of stock that is necessary to achieve some measure of control over the subject corporation. The average control premium in 2024, according to the 2025 Factset Review was 43.8%.

A control premium is calculated by subtracting the minority-interest value of the subject stock from the acquisition price of the subject stock, and then dividing the result by the minority-interest value of the subject stock. When the subject stock is publicly-traded, the minority-interest value is the publicly-traded stock price per share, while the acquisition price is the price per share paid in the acquisition.

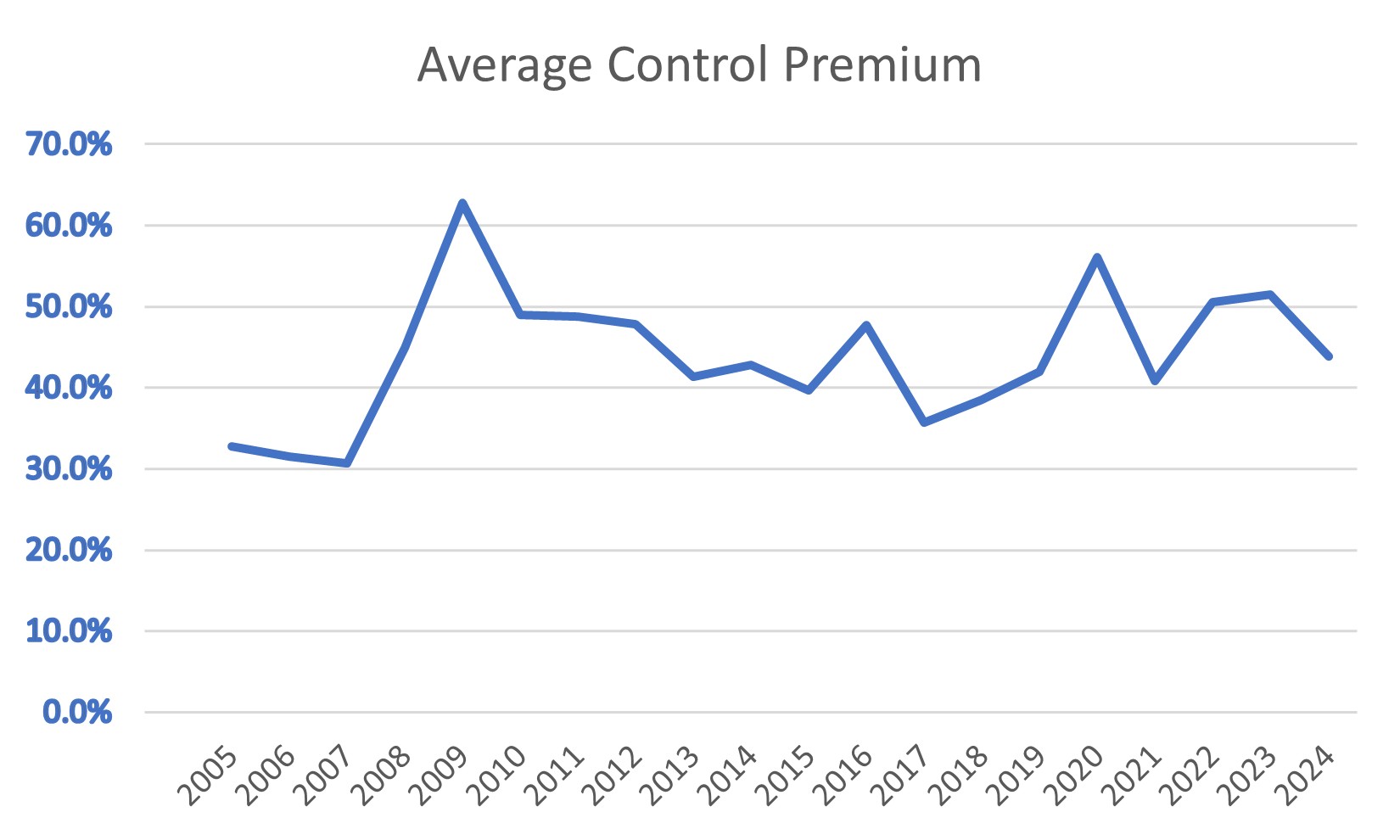

The chart below shows the trend in the average control premium from 2005 to 2024 as reported by Factset.

|

The chart shows that the average control premium was fairly steady over the subject period with a low of 30.7% in 2007 and a high of 62.8% in 2009. Historically, control premiums have fluctuated based on economic conditions, regulatory environments, and industry-specific factors.

The control premiums seem to correlate with the recession at the end of 2007 and its ending in June 2009. Stricter antitrust laws can cause control premiums to decrease, while deregulation can cause control premiums to increase. Industry-specific factors can also influence the size of the control premium. For instance, increased competition in an industry can cause control premiums to increase.

Relevant Court Cases

-

In re the Marriage of David Alan O'Brien

and Cori Lynn O'Brien,

Court of Appeals of Iowa,

No. 24-1853,

filed January 7, 2026

-

Greg Herrick and Jane Evans v. 21st Century

Farms, LTD., and Thomas W. Evans and George

J. Evans, Individually,

Court of Appeals of Iowa,

No. 25-0377,

filed January 7, 2026

Recent Business Valuation Articles

-

“Effects of Long Cycles in Cash

Flows on Present Value,”

by Peter N. Bell,

written January 5, 2026

-

“Introducing the Net Present

Value Profile,”

by Peter Bell,

posted February 19, 2026

Recent Engagements

- Valuation of member interests

of a specialty manufacturer

on a minority interest basis

for gift tax reporting/purchase

purposes.

- Valuation of units of a niche

leasing company on a minority

interest basis for estate tax

reporting purposes.

- Valuation of non-voting

common stock of a manufacturing

company on a minority interest

basis for gift tax reporting

purposes.

- Consulting regarding 100% of

the member interests of a niche

retail and rental firm on a

controlling interest basis for

planning purposes.

";

"

";

" ";

"

";

" ";

"

";

" ";

"

";

" ";

"

";

" ";

";